The systemic risk buffer can be used if there are systemic risks that are not addressed by other macroprudential instruments, like the countercyclical capital buffer or the O-SII buffer. The buffer can both be used to address general systemic risks or risks related to a subset of bank exposures.

Systemic risk buffer

As of 2021 it has become possible to set a systemic risk buffer for Danish banks.

The Systemic Risk Buffer

Purpose

The systemic risk buffer can be used if there are systemic risks that are not addressed by other macroprudential instruments, like the countercyclical capital buffer or the O-SII buffer. The buffer can both be used to address general systemic risks or risks related to a subset of bank exposures.

General systemic risks can be related to the size of the sector, exposure concentrations, a high degree of interconnectedness or a larger risk for contagion given a negative shock to the economy.

It is also possible to use the buffer to address risks related to a subset of exposures, e.g. risks related to lending to a certain industry or a specific geographic region. The European Banking Authority, EBA, has published guidelines for setting a sector specific systemic risk buffer.

The Systemic Risk Buffer

The Council's role

The Council can recommend the activation of the systemic buffer, if the Council finds that there are systemic risks not addressed by other macroprudential tools.

It is the Minister of Industry, Business and Financial Affairs that can activate the systemic risk buffer, and either comply with a recommendation by the Council or explain why the recommendation is not followed.

The Systemic Risk Council (‘the Council’) has on 3 October 2023 recommended to the Minister for Industry, Business and Financial Affairs to activate a sector-specific systemic risk buffer for exposures to real estate companies at a rate of 7 percent, applicable from 30 June 2024.

See below for the Council's latest statements on the systemic buffer.

- Read recommendation on activation of a sector-specific risk buffer for corporate exposures to real estate companies

- Read recommendation of the review of the sector-specific systemic risk buffer

- The Danish Systemic Risk Council’s considerations when setting a sector-specific systemic risk buffer for exposures to commercial real estate companies

- The European Commission’s authorisation of the adoption of a sector-specific systemic risk buffer for corporate exposures to real estate companies

The Systemic Risk Buffer

Legal basis

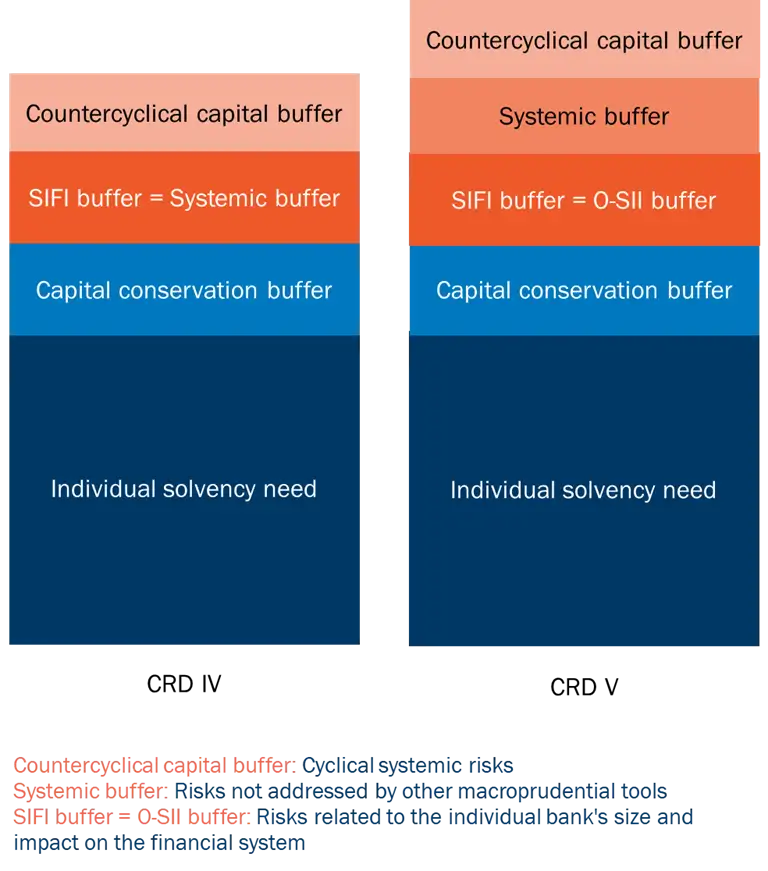

The implementation of the Capital Requirements Directive, CRD V, in Denmark, has led to a number of changes to the capital buffer framework, including the systemic risk buffer and the buffer for other systemically important institutions, O-SII buffer, https://www.retsinformation.dk/eli/lta/2020/2110.

Earlier, the systemic risk buffer was used to set the individual SIFI-buffer requirements in Denmark. With the implementation of the CRDV, the O-SII buffer will be used to set the individual SIFI-buffer requirements. It will thus become possible to set a separate systemic risk buffer, see chart below.

Activating a general or sector-specific systemic risk buffer will as a starting point only apply to banks under Danish supervision. That means that foreign branches and lending directly from banks outside Denmark would not be affected by activating a systemic risk buffer in Denmark. The Danish authorities will have to seek reciprocity with foreign authorities, see also Reciprocation of macroprudential measures.